- Risk switching to enhance popular portfolios like 60-40, Tobias, permanent folio....

- Risk switching to enhance market timing for short term technical trading.

- Risk switching in Intra-Asset class instead of inter-asset class (like stocks & bonds).

- Risk switching with Forex etc.

I use a proprietary portfolio modelling and management software to do the tests. Recently I added couple of new functionalities to that software and this series is a good test for those new capabilities. I created this software over time using C# and R languages to assist in my trading and investigations.The primary driving factor for creating this software is to have ability and flexibility to model multiple types and combinations of diversification (asset, strategy, time & concept), flexibility to incorporate custom money management algorithms, deep analytic at each level (i.e., setup, strategy, portfolios, account level) and other usual stuff. You will find some of those new forensics in this post. Another reason for developing this software - I miss working on technology and this helps. By the way, I have no plans to sell the software. So my reason for sharing above background info is mostly because I feel nice about it.

Risk on - Risk off

Basically this means to me that when the market switches to "Risk on" mode, certain markets go up in price and others go down. The situation reverses in risk off mode. This risk switch is the key driver of everything right now. In this market, either you stay on the right side of the risk switch, or you lose money. Whatever the investment/trading strategy is, IMO having a macro theme behind us to propel the strategy forward to bigger profits is a good idea.

Some may not agree but I think this macro theme (Risk on - Risk off) will be here for a while. Not just because of central banks interventions like QE stuff but my guess is, also because of structural changes happening like proliferation of ETFs contributing to high correlations between assets etc. If interested, you can find my reasoning more on this here. Feel free to disagree. The more our views differ, the better.

Permanent Portfolio

Lately we hear quite a bit about Harry Browne Permanent Portfolio and how this simple portfolio trounced the stock market returns with much lower volatility. If needed, you can find more information about Permanent Portfolio at above wikipedia link. Gist of it is to divide the portfolio into 4 equal parts and invest in the following - 25% Stocks, 25% Bonds, 25% Gold and 25% Cash.

Which Benchmark to use?

Now before we can evaluate whether Risk switching adds value (because of macro theme), we need to decide what would be a good benchmark to measure against. I thought of using SP500 but finally decided to use Permanent Portfolio Mutual fund PRPFX as benchmark.

My reasons - PRPFX returns are much better than SP500 creating a bigger hurdle for Risk Switching to prove it can provide additional profits. Another reason, the fund has price history and is managed professionally to replicate Permanent Portfolio.

Now one problem with PRPFX fund is it also invests in assets like silver, swiss francs, foreign real estate etc to replicate Permanent Portfolio concept. May be it is ok for a professionally managed fund but I am not sure that is a good idea for a retail investor especially for an investment portfolio. So the challenge is how do we replicate PRPFX performance using highly liquid assets that are closer to center field.

For the test, I was able to come up with a portfolio composed of highly liquid assets with performance quite close to PRPFX fund and has correlation above .80. Another reason for coming up with the portfolio is so that we use same assets (and similar weighting) but apply Risk Switching to prove our-selves whether it really enhances the performance.

Portfolio Construction:

Buy and hold following ETFs with investments in each asset according to portfolio percentages mentioned below.

- SPY - 15%, IWM -10%, , SHY - 15%, GLD - 30%, TLT - 30%

Caveats -

Results are frictionless i.e., no commissions and slippages. All calculations are done using monthly data (specifically close of the month). So if there is a severe drop in the middle of the month but with a higher close then that middle of the month drop will not be reflected in drawdown numbers. This applies to all assets and also to the benchmark.

Summary:

- Benchmark = PRPFX

- Portfolio Assets = SPY, IWM, SHY, GLD, TLT

- Portfolio Percentages = 15%, 10%, 15%, 30%, 30%

Risk Switching meets Permanent Portfolio

Portfolio Construction:

The portfolio will be invested in the same assets as above (i.e., SPY, IWM, SHY, GLD, TLT). For the test, the assets are classified as follows:

- Risk-On Assets:: SPY, IWM, GLD, SHY

- Risk-Off Assets:: TLT

Risk Switching Rules:

Each weekend do the following:

- For each Risk-On asset (i.e., SPY, IWM, GLD, SHY), buy (or continue to hold) for next week if it meets following two rules.

- Current week close of Risk-On asset (example: SPY) is higher than its close 13 weeks ago AND

- Last 13 weeks rate of change of Risk-On asset is greater than last 13 weeks rate of change of Risk-Off asset (i.e., TLT).

- Portfolio percentage to invest in each Risk-On asset -- 25%.

- Sell a Risk-On asset and invest the proceeds in TLT (Risk-Off) if the following two rules are met:

- Current week close of TLT is higher than its close 13 weeks ago AND

- Last 13 weeks rate of change of TLT is greater than last 13 weeks rate of change of Risk-On asset.

- Buy SPY (i.e., Risk-On asset) & Sell TLT, if

- Close(SPY) > Close (SPY, 13 weeks ago) AND

- ROC(SPY, 13 weeks) > ROC(TLT, 13 weeks)

- Buy TLT & Sell SPY, if

- Close(TLT) > Close (TLT, 13 weeks ago) AND

- ROC(TLT, 13 weeks) > ROC(SPY, 13 weeks)

- The results are frictionless i.e, no slippage and commissions. On average, the strategy yields around 7 trades per year. So commissions might not be a big factor.

- When switching between Risk-On and Risk-Off (TLT) assets, the test requires there is at least a 1 week delay. In other words, if this weekend our rules tell us to switch from SPY to TLT then we go ahead and sell SPY on Monday. But we will not buy TLT this week. TLT will be bought following week if the switch rule is still in effect. This will cost us some profits but is more realistic.

- The equity curves for this test are closed-equity curves i.e., profits and losses are calculated only after a position is closed. Most investment material uses open-equity curves. I don't use open-equity in my trading and have not yet developed fully in the software. If any reader tries out above rules and creates open-equity curves then I appreciate if you can share your findings in comments section.

Summary:

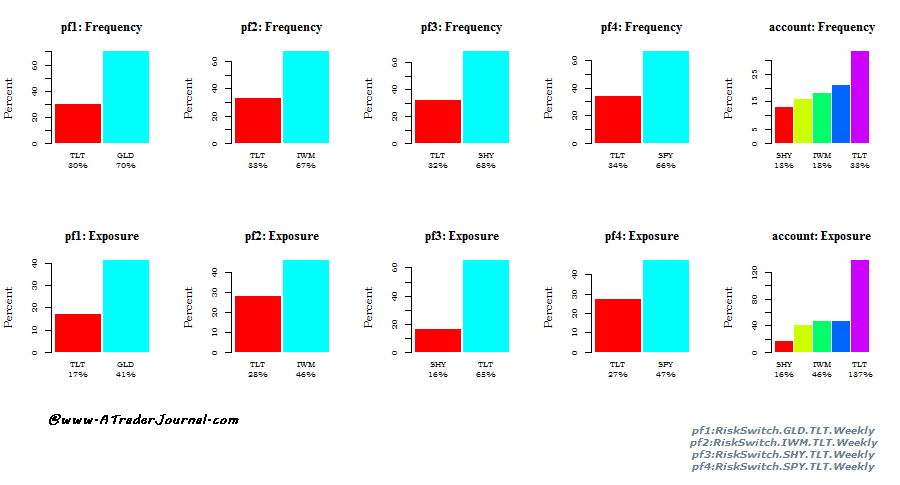

Above annotated images provides various performance stats and forensics into the portfolio. Each of the stats provide wealth of information not only on this strategy but also provide some idea of what to expect when doing Risk On - Risk Off in general. But going through all stats will make this already long post a very looong post.

So I am going to just summarize few key points and let readers comment on stats that catch their attention.

- Stats indicate Risk Switching do enhance the Permanent Portfolio returns.

- The enhancement of returns appear mostly because of over exposure to TLT. You can see that in portfolio frequency and exposure graphs.

- Currently TLT is a good proxy for implementing Risk Switching but it may not be in future. One way to make the Risk Switching layer robust is to do switching only if the designated Risk Off asset has low correlation to Risk On asset over a specified time frame.

- Not all assets relate well for risk switching with TLT. For example, the analytics graphs and performance summary tables clearly indicate GLD and TLT don't play well. That makes sense. Same for TLT and Cash.

- From the analytics table - Risk Switching with SPY has 78% win rate. This seems to be a good timing indicator. One area to investigate - can we use this as a timing indicator for short term technical trading of SPY or ES?

- Similarly IWM has excellent risk:reward profile when it comes to Risk Switching with TLT. It does not have as high win% as SPY but still 67% is a good win rate. I thought IWM will have better win% then SPY as SPY represents only big cap stocks which in general are less volatile then stocks in IWM.

0 comments:

Post a Comment